401(k) & IRA Withdrawal Tax Calculator

Enter your account details to estimate taxes, check RMD requirements, and see your net after-tax withdrawal.

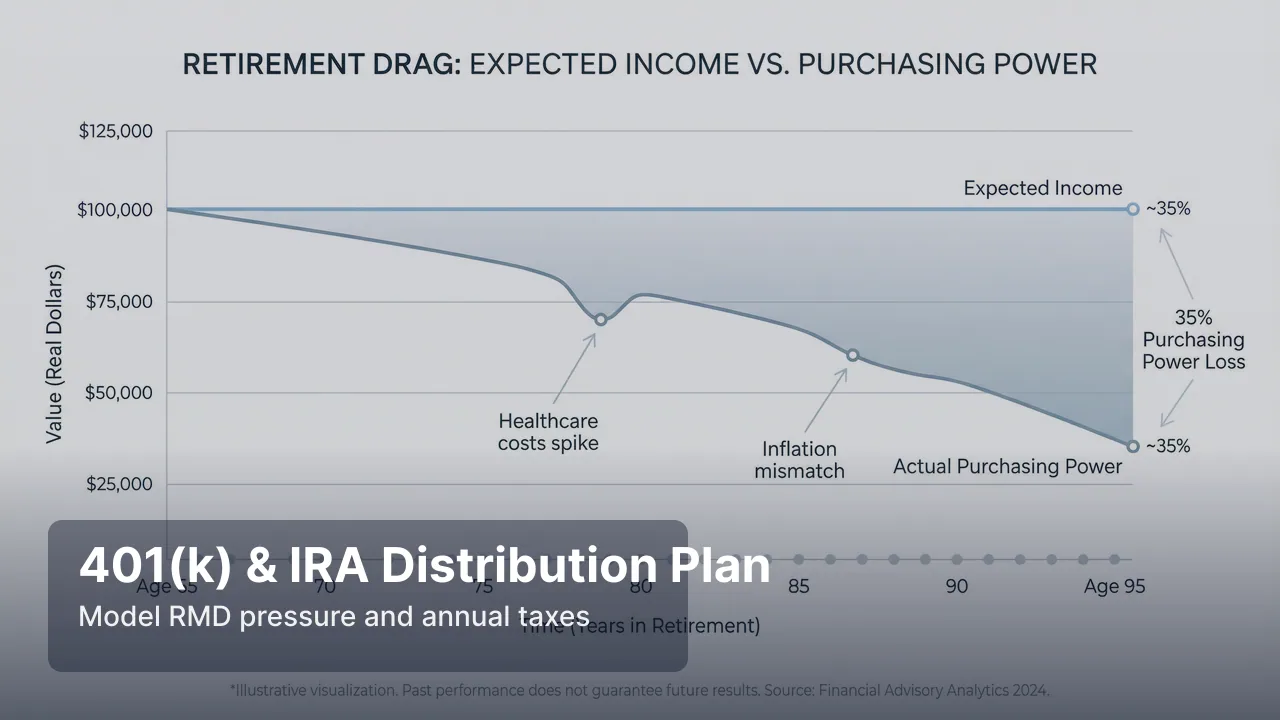

How RMD Pressure Connects to Roth Strategy

RMD pressure builds quietly: each year past 73, the IRS Uniform Lifetime Table forces a larger slice of your Traditional balance out. Pre-RMD Roth conversions can defuse that pressure — but the right conversion size depends on your bracket fill, the years remaining, and your IRMAA exposure. The full Praxion plan models that interaction for your inputs.

Model RMD + Roth strategy in the full plan →Why 401(k) and IRA Withdrawal Planning is Critical

Traditional retirement accounts eventually trigger taxable withdrawals, and poor timing can push retirees into higher tax brackets. Coordinating withdrawal amounts before and after RMD age helps reduce tax shocks.

What to Calculate

- Expected annual distributions from 401(k) and IRA balances

- Projected tax impact by bracket year-over-year

- RMD-driven income increases and downstream tax effects

- How Roth conversions can reduce future RMD pressure

RMD Planning and Conversion Windows

Many retirees have a lower-tax window after employment ends and before RMDs begin. This period can be used for strategic conversions and bracket management.

Pair this analysis with the Roth Conversion Calculator to evaluate annual conversion ranges.

Research References

RMD timing and IRA distribution treatment in this planning flow are based on IRS retirement-plan guidance and IRA publications.

Sources: IRS RMD Guidance, IRS Publication 590-B, IRS 2024 RMD Rule Update.

Internal Planning Path

- Start with Roth Conversion Calculator

- Compare sequencing in Withdrawal Strategy

- Validate total tax impact in Retirement Tax Planner