1. Introduction — Retirement Readiness

Retirement is one of life's biggest financial milestones. The Can I Retire? tool helps evaluate the modeled financial situation, map retirement income, and highlight modeled gaps toward a comfortable, secure retirement.

Whether early in a career, in mid-life, or approaching a target retirement age, this tool provides modeled insights based on:

- Current savings and investment balances

- Expected retirement income streams

- Social Security benefits

- Lifestyle and anticipated expenses

2. How the Tool Works

Our calculator takes key inputs including:

- Current age and desired retirement age

- Savings in retirement accounts (401k, IRA, brokerage)

- Expected Social Security benefits

- Annual expenses in retirement

- Part-time income, pensions, or other income

Based on these inputs, the tool calculates:

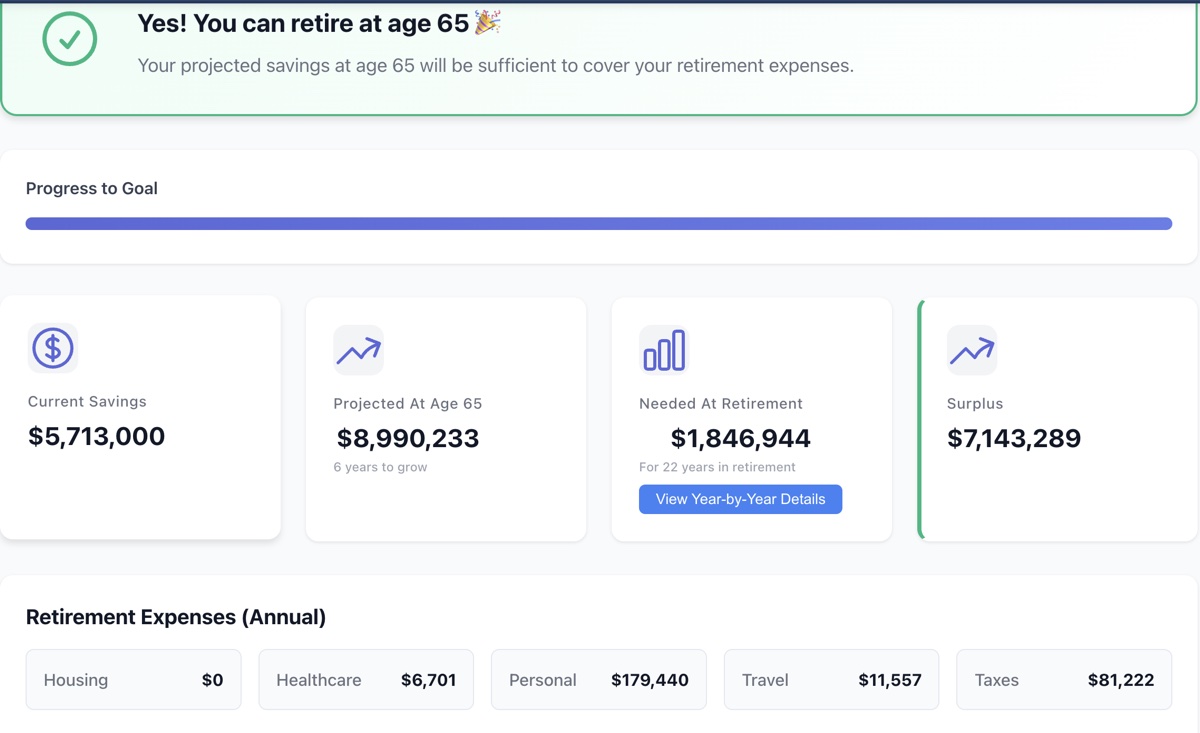

- Retirement readiness score – modeled probability of retiring comfortably

- Annual sustainable withdrawals – how much the model indicates can be withdrawn per year

- Savings gap – whether current savings and plans cover projected retirement expenses

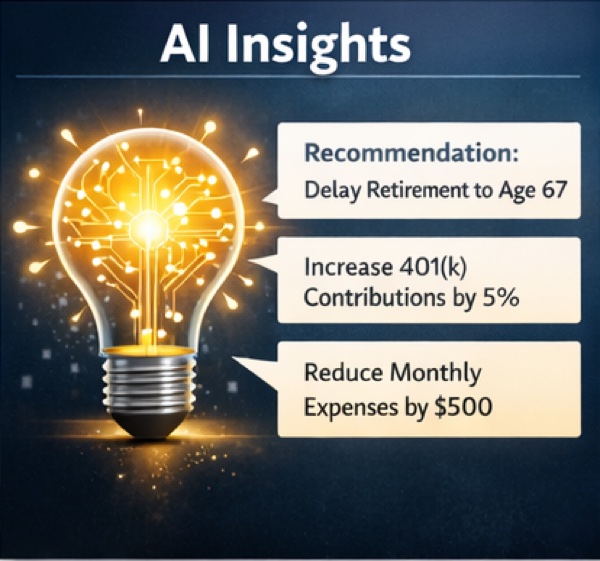

💡 AI Insight

After inputs are entered, the tool can generate personalized modeled suggestions, such as increasing contributions, adjusting retirement age, or analyzing the investment mix.

3. Key Retirement Planning Concepts

3.1 Social Security Timing

The age at which Social Security benefits are claimed affects the monthly payment. Claiming early reduces monthly payments, while delaying can increase them. Consider health, life expectancy, and retirement savings before deciding.

3.2 Healthcare Costs & Medicare

Healthcare costs can make up a significant portion of retirement expenses. Planning for Medicare eligibility at age 65 and potential supplemental coverage is crucial.

3.3 Tax-Efficient Withdrawals

Withdrawal order matters:

- Taxable accounts

- Tax-deferred accounts (401k, Traditional IRA)

- Tax-free accounts (Roth IRA)

Proper sequencing can reduce lifetime tax burden.

3.4 Inflation & Cost of Living

A dollar today won't be worth the same in 10–30 years. Include inflation assumptions in planning so modeled retirement income maintains purchasing power.

3.5 Emergency & Contingency Planning

Unexpected expenses like market downturns, healthcare emergencies, or family obligations should be factored in. The tool assumes a conservative safety buffer to model these scenarios.

4. Using AI to Model the Retirement Plan

After using the calculator, AI-generated suggestions appear as follows:

- Suggested contribution adjustments

- Potential retirement age scenarios

- Ways to reduce spending or increase income streams

- Suggested account withdrawals to minimize taxes

Example:

"Based on the inputs entered, retiring at 65 may leave a $20,000 annual shortfall. The model suggests either delaying retirement by 2 years or increasing 401(k) contributions by 5%."

5. Advanced Retirement Considerations

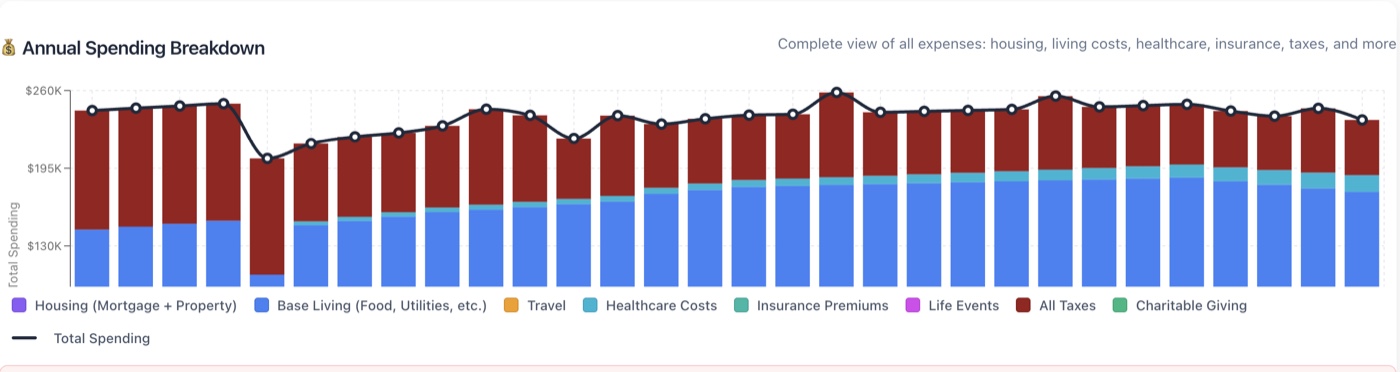

5.1 Monte Carlo Simulation & Market Variability

Market returns fluctuate, which affects retirement savings. Using Monte Carlo simulations helps estimate outcomes under different market conditions and risk levels.

5.2 Longevity & Life Expectancy

Planning for a longer life helps ensure funds don't run out in the model. Consider family history, health, and lifestyle when estimating retirement duration.

5.3 Part-Time Work or Side Income

Even limited income after retirement can reduce withdrawal pressure on savings and increase financial flexibility.

5.4 Real Estate & Other Assets

A home or other assets can serve as retirement resources (e.g., downsizing, reverse mortgages). Include these in retirement calculations where appropriate.

5.5 Debt & Liability Management

Paying off high-interest debt before retirement reduces monthly obligations and improves retirement readiness.

6. Tips for Maximizing Retirement Readiness

- Start early: Even small contributions today grow significantly over decades.

- Diversify investments: Balance risk and reward across accounts.

- Plan Social Security strategically: Evaluate early vs. delayed claiming.

- Account for inflation: Expenses will increase over time.

- Monitor and revisit annually: Life changes and market shifts require updates.

- Consider professional advice: Financial planners or CFPs can provide personalized guidance.

7. FAQs — Common Questions About Retirement Planning

Q1: What is a safe withdrawal rate?

A common guideline is 4% annually, but it varies depending on retirement length, market returns, and inflation.

Q2: How much do I need to retire comfortably?

This depends on desired lifestyle, expected expenses, and income sources. The tool calculates a personalized gap and readiness score from the inputs.

Q3: Can I retire early with limited savings?

Early retirement is possible but may require adjustments to spending, income, or retirement age. AI insights provide actionable strategies.

Q4: How often should the retirement plan be updated?

At least once a year, and whenever major life events occur (new job, inheritance, health changes).

8. Next Steps

- Run the Tool Now: Enter inputs and view the retirement readiness score.

- Download the Personalized Plan: Save results and AI-generated analysis.

- Explore Further Guidance: Check our:

Ready to Check Retirement Readiness?

Create a free account to access this tool and assess retirement readiness with the comprehensive calculator.