Most articles explain why rebalancing matters. Far fewer explain how to do it when taxes, multiple accounts, and long-term holdings are involved.

This article focuses on practical, tax-aware rebalancing — the version investors actually need.

Does rebalancing trigger capital gains?

Short answer: only when you sell an appreciated holding in a taxable brokerage account. Rebalancing inside a 401(k), Traditional IRA, or Roth IRA is never a taxable event — you can buy and sell freely. In a taxable account, selling a fund or stock that has gained value realizes a capital gain (long-term if held more than a year), which is taxed that year. The rest of this guide shows how to rebalance while minimizing — or entirely avoiding — those gains.

What This Article Covers

This guide explains how to rebalance a portfolio in a tax-aware way when investors have multiple accounts, large unrealized gains, and long-term holdings they prefer not to sell. The focus is on reducing risk while minimizing unnecessary tax consequences.

What Traditional Rebalancing Gets Right — and What It Misses

Classic finance theory suggests that investors should periodically restore their portfolios to a target mix of stocks and bonds in order to:

- Maintain a consistent level of risk

- Prevent overexposure after market rallies

- Enforce discipline during volatile periods

This logic is supported by decades of academic research, including work from:

- Vanguard

- Morningstar

- CFA Institute

However, most theoretical models assume:

- A single account

- No taxes

- No emotional or legacy holdings

That is not how most people invest.

The Real-World Portfolio Problem

In practice, investors often have:

- Multiple brokerage accounts

- 401(k)s, IRAs, and Roth IRAs

- Individual stocks, ETFs, and mutual funds

- Large unrealized capital gains

- Different tax treatments across accounts

A rigid "sell and rebalance" approach can:

- Trigger unnecessary capital gains taxes

- Increase Medicare surtaxes (NIIT)

- Create avoidable state tax exposure

- Reduce long-term after-tax returns

This is why many investors know rebalancing matters — but avoid doing it.

What This Guide Covers

This article explains how to rebalance an investment portfolio in real-world conditions, including:

- Multiple taxable and tax-advantaged accounts

- Large unrealized capital gains

- Long-term holdings investors don't want to sell

- Tax-aware decision-making across a household portfolio

It is designed for investors who want to reduce risk without triggering unnecessary taxes.

What the Research Actually Supports

Major investment research organizations increasingly emphasize tax-aware portfolio management rather than mechanical rebalancing.

For example:

- Vanguard promotes cash-flow-based rebalancing using new contributions

- Morningstar highlights the importance of tolerance bands rather than fixed targets

- The CFA Institute acknowledges that taxes materially affect portfolio outcomes

The takeaway is clear:

Risk control matters — but taxes matter too.

How to Rebalance a Portfolio Tax-Efficiently (Step-by-Step)

Rather than asking "How do I rebalance perfectly?", investors can ask:

"How do I reduce risk with the least tax friction?"

The following steps outline a practical, tax-efficient approach to portfolio rebalancing used by advisors and supported by academic research.

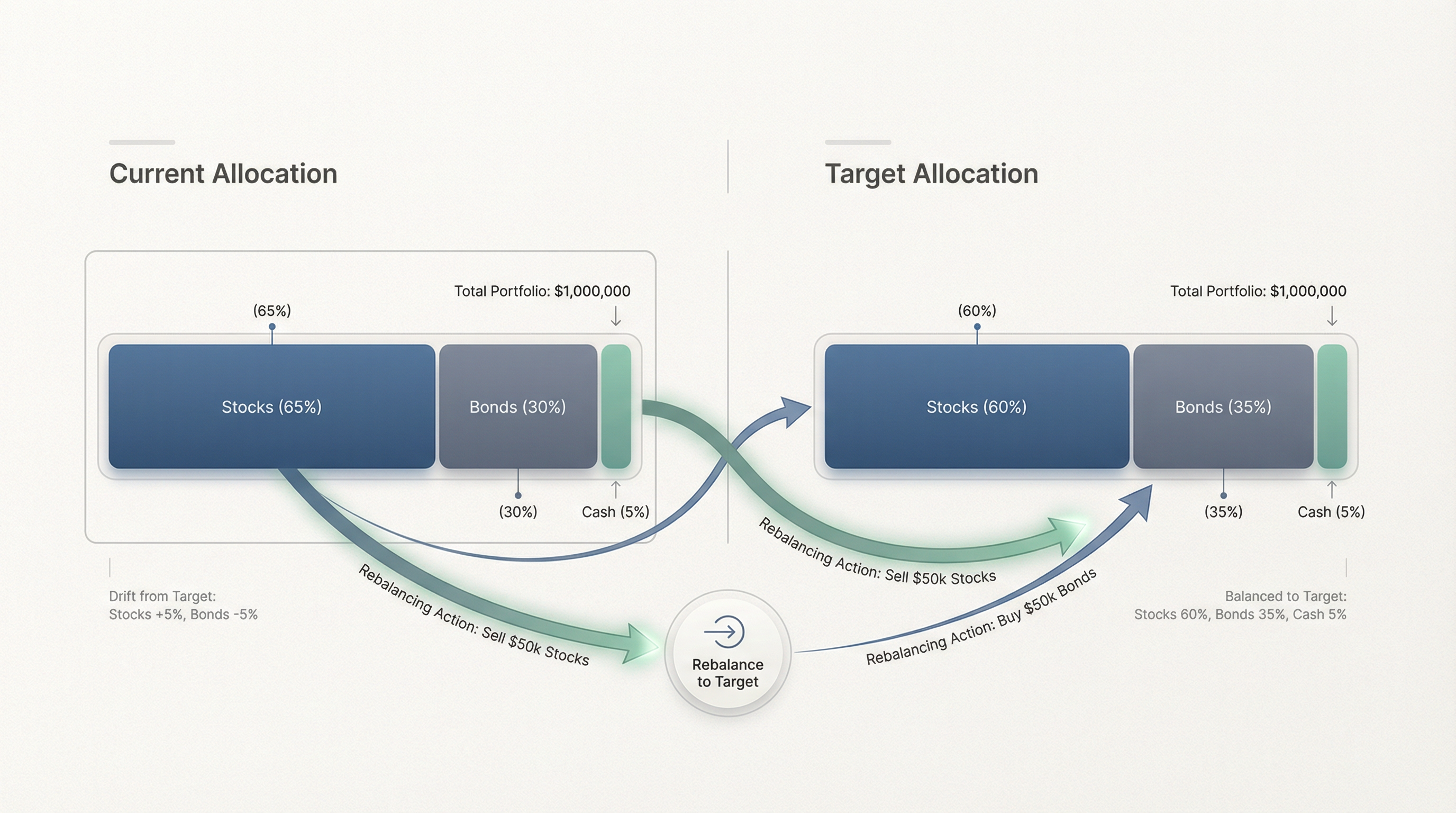

Step 1: Set Allocation Ranges Instead of Exact Targets

Instead of aiming for precision, use allocation ranges.

Example:

Target: 70% stocks / 30% bonds

Acceptable range:

- Stocks: 60%–80%

- Bonds: 20%–40%

This approach:

- Reduces unnecessary trading

- Avoids taxes triggered by minor market moves

- Reflects how risk actually behaves

Morningstar and Vanguard both support range-based approaches for long-term investors.

Step 2: Use Cash Flows to Rebalance Without Selling

The most tax-efficient rebalancing tool is new money.

This includes:

- New contributions

- Dividends

- Interest payments

Directing cash flows into underweighted assets can gradually rebalance a portfolio without selling existing holdings.

This approach is widely recommended by:

- Vanguard research

- Fidelity investor education

- Bogleheads investment philosophy

Step 3: Rebalance Inside Tax-Advantaged Accounts First

When adjustments are required, many households prioritize trades inside tax-advantaged accounts whenever possible.

Examples:

- 401(k)s

- Traditional IRAs

- Roth IRAs

Trades inside these accounts typically:

- Do not trigger capital gains taxes

- Allow flexibility to offset taxable account concentration

This allows investors to rebalance at the household level, even if individual accounts look unbalanced.

Step 4: Allow Controlled Drift When Capital Gains Are High

Controlled drift is not negligence — it is strategy.

Allowing a portfolio to remain slightly overweight in stocks may be reasonable when:

- Gains are large and long-term

- The investor remains within acceptable risk bounds

- Selling would materially reduce after-tax returns

This concept is discussed in tax-efficient investing literature from:

- CFA Institute publications

- Vanguard's Advisor Alpha framework

Step 5: Sell Strategically When Rebalancing Is Required

Sometimes selling is unavoidable:

- Risk exceeds acceptable limits

- Life events require liquidity

- Retirement income planning begins

When selling is required, common techniques include:

- Selling highest cost-basis shares first

- Favoring long-term over short-term gains

- Coordinating with available capital losses

- Monitoring income thresholds that affect tax rates

This is not "market timing" — it is tax-aware tradeoff analysis.

Tax Context: The 3.8% Net Investment Income Tax (NIIT)

One tax that materially affects rebalancing decisions for mass-affluent households is the Net Investment Income Tax (NIIT) — a 3.8% surtax on investment income (interest, dividends, capital gains, rental income, royalties) above certain MAGI thresholds.

- Threshold (single): $200,000 MAGI

- Threshold (married filing jointly): $250,000 MAGI

- Surtax rate: 3.8% on investment income above the threshold (or on the amount your MAGI exceeds the threshold, whichever is smaller)

Important detail: these thresholds have been frozen since 2013 — they are not indexed for inflation. As wages and portfolio balances grow over time, more mass-affluent households are pulled into NIIT each year without any change in their actual lifestyle.

For rebalancing, this means a sale that triggers a $50,000 long-term capital gain can carry an effective tax rate of 15% (LTCG) plus 3.8% (NIIT) = 18.8% federal, not just the 15% the quick-math LTCG bracket implies. State taxes stack on top of that. Coordinating sales with low-MAGI years — or absorbing the gain inside tax-advantaged accounts where the trade doesn't hit NIIT — is the practical response.

Asset Location: Where You Hold Each Asset Matters As Much as What You Hold

Asset allocation is the mix of stocks, bonds, and cash across the entire portfolio. Asset location is which type of account each asset sits in. The two concepts are routinely conflated, but for tax-aware investors they are the highest-leverage decision after allocation itself.

The general framework most practitioners follow:

| Account type | Often best suited for | Why |

|---|---|---|

| Taxable (brokerage) | Broad-market equity index funds and ETFs; municipal bonds | Long-term capital gains and qualified dividends taxed at preferential rates; index ETFs distribute few capital gains; munis are federally tax-free interest. |

| Traditional IRA / 401(k) | Bonds and bond funds; REITs; high-turnover active funds | Ordinary-income rates apply on withdrawal anyway, so high-tax-drag assets (bond interest, REIT distributions, short-term gains) cause no extra harm here. |

| Roth IRA / Roth 401(k) | Highest-expected-return assets (small-cap, emerging markets, growth equity) | All gains compound tax-free and come out tax-free in retirement — concentrate the highest expected returns here. |

Asset location is a framework — household-specific factors (tax bracket, withdrawal sequencing, legacy goals, existing concentrations) change the optimal placement. Treat the table as a starting heuristic, not a rule.

Why it matters for rebalancing: if your bonds are inside the 401(k), you can rebalance them freely without triggering any taxable event. If your bonds sit in the taxable account, every rebalancing trade triggers interest, ordinary-income tax, and potentially NIIT. Putting tax-inefficient assets in tax-advantaged accounts often does more for long-term after-tax returns than fine-tuning the allocation itself.

Direct Indexing and SMA Tax-Loss Harvesting

For households with substantial taxable assets (typically $500K+ in a single account), direct indexing — sometimes delivered through a separately managed account (SMA) — is an alternative to holding a single index fund. Instead of owning one ETF that tracks the S&P 500, the account holds the individual underlying stocks. The implementation is the same exposure; the tax mechanics are different.

- Systematic loss harvesting at the individual security level. When any single stock falls below cost basis, the manager can sell it, take the loss, and immediately buy a non-substantially-identical replacement that preserves index exposure. Losses become available to offset gains elsewhere in the portfolio.

- More harvesting opportunity than a single ETF. A broad-market index ETF rarely shows a loss in a positive-trend year because winners offset losers inside the fund. Direct indexing exposes the dispersion underneath, so even in a year the index is up, dozens of individual stocks may be down — each a harvesting opportunity.

- Practical tradeoffs. Direct indexing typically carries higher fees than an index ETF (often 25–40 basis points / 0.25–0.40% vs. 3–5 bps for a broad-market ETF), complex tax-lot accounting that can complicate brokerage transfers, and concentration constraints if you have appreciated single stocks you do not want to sell. The fee differential is usually justified only when harvested losses exceed the fee drag — typically requiring meaningful capital gains elsewhere in the portfolio to absorb.

- Best fit: households with large taxable balances, regular realized gains from concentrated positions or business sales, and a long enough horizon for accumulated loss carryforwards to be useful.

Concentrated Stock Positions: Tax-Aware Rebalancing for HNW Investors

For high-net-worth households, a single concentrated position (often appreciated employer stock, a founder's shares, or a long-held growth name) is frequently the largest line item on the balance sheet. Standard rebalancing advice — "sell down the overweight, rebalance to target" — runs into two HNW-specific tensions: the embedded capital-gains tax can be a meaningful percentage of the position's value, and concentration itself amplifies portfolio volatility in ways the household's risk tolerance was probably not modeled against.

The volatility math worth knowing:

- A single stock typically carries 25–40% annualized volatility vs. roughly 15–18% for a broad index.

- When that stock is also 30%+ of the household portfolio, the household's effective equity volatility meaningfully exceeds what their target allocation implies.

- The asymmetric downside (a single-stock 50% drawdown) can be a portfolio-wrecker that no rebalancing schedule will recover from quickly — especially close to or in retirement.

Practitioner-standard tax-aware unwind tactics (most useful when used in combination, not in isolation):

- Exchange funds (Section 351 / Section 721 vehicles) — contribute the concentrated position to a pooled fund in exchange for a diversified basket without realizing a gain. Multi-year lockup (typically 7 years) and accredited-investor requirements apply.

- NUA (Net Unrealized Appreciation) on employer stock — for company stock held inside a 401(k), a lump-sum distribution can be structured so the appreciation is taxed as long-term capital gains rather than ordinary income at withdrawal. Highly specific eligibility rules; works once per employer.

- Charitable Remainder Trusts (CRTs) — gift the position to a CRT, get an income stream for life plus a partial charitable deduction, and the trust sells the position tax-free. Useful when charitable intent is genuine and the position is large enough that the structure pays for itself.

- 10b5-1 trading plans (for insiders) — pre-committed selling schedule that allows executives subject to trading windows to systematically unwind without running afoul of insider-trading rules.

- Completion portfolio via direct indexing — leave the concentrated position untouched and build a diversified portfolio in the rest of the account that explicitly under-weights the concentrated stock's sector / factor exposure. Reduces net concentration without realizing gains.

Practical heuristic: don't unwind faster than the tax-loss harvest budget can absorb the gain. If the concentrated position has $500,000 of unrealized gain and the rest of the portfolio generates roughly $30,000–$50,000 of harvestable losses per year via direct indexing, the natural unwind cadence is multi-year (5–10 years), not all-at-once. Combine with the NIIT context above — a sale that triggers a long-term capital gain in a year your MAGI already exceeds $250,000 for MFJ filers carries an additional 3.8% NIIT on top of the LTCG bracket.

Concentrated-stock unwinds are one of the more complex personal-tax planning situations and the right structure depends heavily on charitable intent, employment status (insider vs. retired), estate goals, and state-tax exposure. Consult a fee-only financial planner and tax professional before committing to any of these tactics.

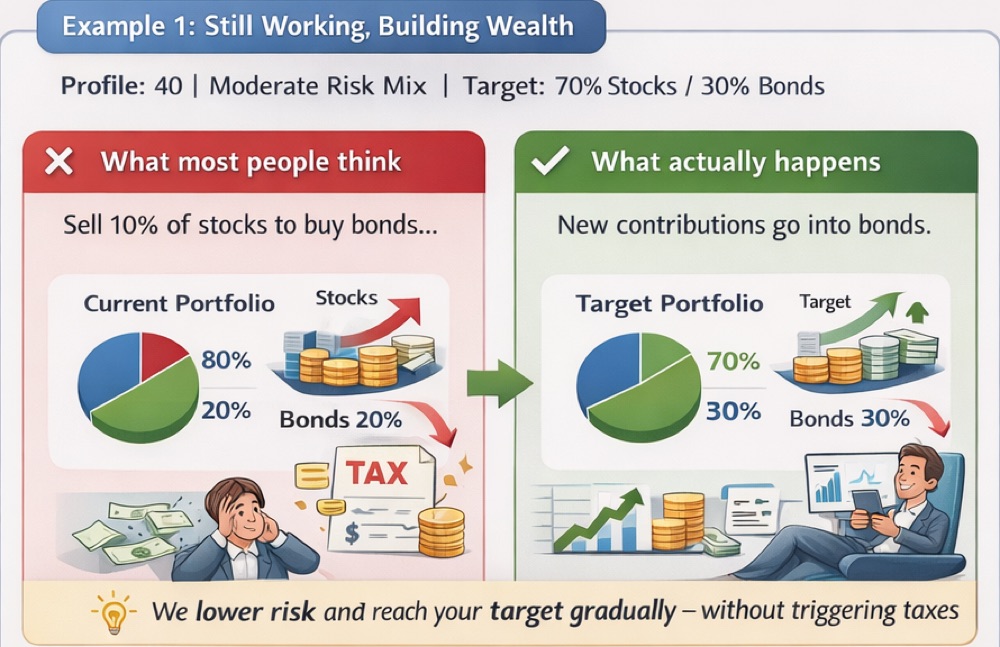

Example: 42-Year-Old Professional With Large Unrealized Gains

Situation

- Portfolio drifted to 82% stocks after a bull market

- Significant long-term capital gains in taxable accounts

- Moderate risk tolerance

Tax-Aware Rebalancing Strategy

- No immediate selling in taxable account

- New contributions directed to bonds

- Dividends reinvested into underweighted assets

Result

- Risk reduced gradually over time

- Capital gains deferred

- Portfolio aligned with long-term plan

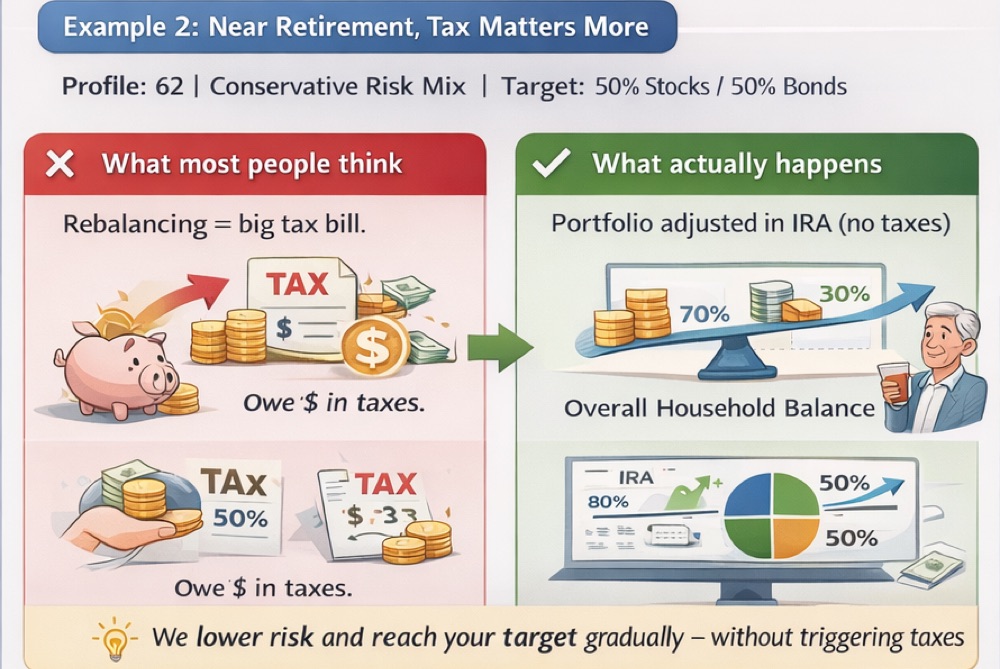

Example: 63-Year-Old Pre-Retiree With Large Taxable Gains

Situation

- Approaching retirement with conservative risk tolerance

- Large unrealized capital gains in taxable brokerage account

- Significant assets in IRA with no tax consequences for trading

Tax-Aware Rebalancing Strategy

- Portfolio rebalanced entirely within IRA (no taxes)

- Taxable holdings left untouched to preserve cost basis

- Overall household allocation brought back into target range

Result

- Risk reduced without triggering capital gains

- Tax-deferred growth preserved in IRA

- Greater retirement readiness and financial flexibility

Who Often Uses This Tax-Aware Rebalancing Approach

This tax-aware rebalancing approach is especially relevant for:

- Investors with both taxable brokerage accounts and retirement accounts (401(k), IRA, Roth IRA)

- Long-term holders with large unrealized capital gains

- Pre-retirees looking to manage risk without triggering unnecessary taxes

- Professionals contributing regularly to investment accounts

- Anyone seeking to improve after-tax returns over time

This strategy prioritizes household-level allocation rather than forcing each individual account to match a rigid target. For more on comprehensive retirement planning strategies, see our complete user guide.

Why This Approach Matters Long Term

Research consistently shows that:

- Taxes are one of the largest drags on long-term returns

- Investor behavior matters more than precision

- Simple, repeatable strategies outperform complex ones over time

A tax-aware rebalancing strategy helps investors:

- Stay invested

- Avoid emotional decisions

- Maintain discipline through market cycles

Common Misconceptions About Rebalancing

"If I don't rebalance exactly, I'm doing it wrong."

→ Staying within a safe range is often sufficient.

"Rebalancing always means selling."

→ Cash flows and tax-advantaged accounts often solve the problem.

"Taxes are secondary to allocation."

→ After-tax outcomes are what investors actually keep.

Key Takeaway

Effective rebalancing is not about perfect allocations — it's about managing risk intelligently while respecting taxes and real-life complexity.

Methodology and Research Foundation

This framework reflects principles supported by leading investment research organizations:

- Vanguard research on cash-flow-based rebalancing and tax-efficient portfolio management

- Morningstar guidance on tolerance bands and practical rebalancing strategies

- CFA Institute publications on tax-aware portfolio management for long-term investors

The approach prioritizes after-tax outcomes, which are the returns investors actually keep. While traditional rebalancing focuses on risk control, this methodology recognizes that taxes represent one of the largest long-term drags on portfolio returns — and should be managed accordingly.

By combining academic research with real-world portfolio constraints, this strategy provides a practical path for investors to maintain appropriate risk levels while supporting wealth preservation over time. For tools to model different rebalancing scenarios, explore our Monte Carlo simulation and tax analysis calculator.

External References & Further Reading

You can explore these authoritative sources for more information:

Frequently Asked Questions

Does rebalancing a portfolio trigger capital gains taxes?

Only when you sell an appreciated holding in a taxable brokerage account. Rebalancing inside a 401(k), Traditional IRA, or Roth IRA is not a taxable event — you can buy and sell freely. In a taxable account, selling a fund or stock that has risen in value realizes a capital gain (long-term if held more than a year, short-term if held less), which is taxed for that year.

How do I rebalance without triggering capital gains?

Four tactics, in order of tax efficiency: (1) direct new contributions, dividends, and interest into underweighted assets so you buy your way back to target without selling; (2) do required selling inside tax-advantaged accounts (401(k), IRA, Roth), where trades are tax-free; (3) allow controlled drift within an allocation band rather than selling for small deviations; and (4) when you must sell in a taxable account, pair the gain with harvested losses and favor long-term lots.

Does rebalancing inside an IRA or Roth IRA cause taxes?

No. Buying and selling inside a Traditional IRA, Roth IRA, or 401(k) does not create a taxable event — no capital gains, dividends, or interest are taxed while the money stays in the account. This is why many households run all of their rebalancing trades inside tax-advantaged accounts and leave appreciated taxable holdings untouched.

What is the difference between tax-aware and tax-optimized rebalancing?

Tax-aware rebalancing treats taxes as one factor while restoring your target allocation — for example, preferring cash-flow rebalancing and trades inside IRAs. Tax-optimized rebalancing goes further and explicitly minimizes the tax bill: coordinating lot selection, loss harvesting, NIIT and bracket thresholds, and multi-year sequencing, sometimes accepting slightly more allocation drift to lower lifetime tax.

Do index funds and ETFs reduce rebalancing taxes?

Partly. Broad-market index ETFs distribute few internal capital gains, so holding them in a taxable account creates fewer surprise taxable events than actively managed funds. But selling an appreciated ETF to rebalance still realizes a capital gain. ETFs help with a fund's internal tax drag — not with the gain you realize when you sell to rebalance.

Editorial Note: This article is for educational purposes only and does not constitute individualized investment or tax advice. Investors should consider their own circumstances or consult a qualified professional.