Social Security Analyzer: Maximize Your Benefits with Smart Planning

Discover your optimal claiming age with tax-adjusted analysis, opportunity cost modeling, and comprehensive retirement planning

Last updated: February 14, 2026

Planning for Social Security can feel overwhelming. With multiple claiming ages, complex tax rules, and strategies to maximize lifetime benefits, it's easy to wonder: When is the best time to claim my Social Security benefits?

That's where a Social Security analyzer comes in—a tool designed to provide clarity, guidance, and confidence in one of your most critical financial decisions. Unlike basic calculators that show generic estimates, a comprehensive analyzer factors in your unique circumstances: life expectancy, tax situation, other income sources, and investment strategies.

Why Timing Matters: The Impact of Your Claiming Age

The age at which you claim Social Security has a dramatic impact on your monthly and lifetime benefits. Here's how claiming age affects your monthly benefit amount:

Social Security Claiming Ages

- Age 62 (Early Claiming): Reduces your monthly benefit by up to 30%, but provides income sooner. Best if you need income immediately or have shorter life expectancy.

- Full Retirement Age (FRA, typically 67): Receive 100% of your calculated benefit. The "baseline" for comparison.

- Age 70 (Maximum Delay): Increases your benefit by roughly 8% per year beyond FRA, maximizing monthly payments. Best for longevity, tax management, or those with other income sources.

Example: If your Full Retirement Age benefit is $2,500/month:

- Claiming at 62: ~$1,750/month (30% reduction)

- Claiming at 67 (FRA): $2,500/month (100%)

- Claiming at 70: ~$3,100/month (24% increase)

💡 It's Not Just About the Numbers

Choosing the right age isn't just about maximizing monthly payments. Factors like your adjusted life expectancy, current savings, tax situation, spousal coordination, and other sources of income all influence which strategy is optimal for your retirement.

How Taxes Affect Social Security Benefits

Here's a critical fact many retirees overlook: up to 85% of Social Security benefits may be taxable. Your tax liability depends on your provisional income, which includes:

- Adjusted Gross Income (AGI)

- Nontaxable interest (e.g., municipal bonds)

- 50% of your Social Security benefits

Social Security Taxation Thresholds

| Filing Status | Provisional Income | Taxable % |

|---|---|---|

| Single | < $25,000 | 0% |

| Single | $25,000 – $34,000 | 50% |

| Single | > $34,000 | 85% |

| Married (Joint) | < $32,000 | 0% |

| Married (Joint) | $32,000 – $44,000 | 50% |

| Married (Joint) | > $44,000 | 85% |

An effective Social Security analyzer factors in these thresholds, ensuring your claiming strategy accounts for taxes and maximizes your after-tax income—not just gross benefits.

⚠️ Tax Planning Opportunity

Strategic timing of Social Security claiming, combined with Roth conversions and withdrawal sequencing, can significantly reduce lifetime taxes. Many retirees leave tens of thousands on the table by not considering tax implications of their claiming decision.

Understanding Opportunity Cost: What You Gain by Waiting

Every decision has trade-offs. By claiming early, you gain immediate income but miss out on the higher benefits that come from delaying. By waiting, you increase monthly payments but forgo years of benefits you could have received (and potentially invested).

What a Social Security Analyzer Calculates

- Benefits received during the delay period: Total income you'd receive by claiming earlier

- Annual benefit increases: How much your monthly payment grows by waiting

- Break-even age: The age at which delayed benefits surpass early claiming

- Investment potential: Value of investing early benefits vs. receiving higher payments later

- Lifetime value: Total benefits over different life expectancies

Example Scenario:

Delaying from age 62 to 70 could increase your lifetime benefits by over $400,000, depending on your life expectancy and investment strategy. However, if you have poor health or limited life expectancy, claiming early and investing the benefits might provide better outcomes.

Break-Even Analysis

If you delay claiming from 67 to 70 (gaining 24% higher monthly benefits), you typically break even around age 80-82. If you expect to live beyond that age, delaying often provides greater lifetime value. If you don't expect to reach that age, claiming earlier may be optimal.

A comprehensive Social Security analyzer shows exactly when you break even under different scenarios and life expectancies.

Praxion Finance's Social Security Analyzer

At Praxion Finance, we've built a Social Security analyzer that goes beyond basic calculators. Our tool integrates with your complete retirement plan to provide:

✓ Personalized Analysis

Tailored claiming strategies based on your adjusted life expectancy, savings, spouse's benefits, and income sources. Not generic averages—analysis specific to your situation.

✓ Break-Even Analysis

Shows the precise age at which delayed benefits surpass early claiming. Visualize cumulative benefits over time and understand exactly when waiting pays off.

✓ Tax Implications

Visualizes how taxes impact your after-tax benefits at different claiming ages. See how provisional income thresholds affect your net income and coordinate with other tax strategies.

✓ Opportunity Cost Analysis

Demonstrates the value of waiting versus claiming early. Models what happens if you invest early benefits versus receiving higher payments later. Shows trade-offs with transparency.

✓ Advanced Scenario Planning

Combine Social Security with your investment portfolio to understand total retirement outcomes. Test different claiming ages alongside withdrawal strategies, Roth conversions, and market scenarios.

With Praxion Finance, you can:

- Compare claiming at 62, 67, and 70 in a single view

- See tax-adjusted monthly benefits for each scenario

- Understand how spousal benefits coordinate with your claiming decision

- Model longevity risk and break-even points

- Make data-driven decisions that align with your overall retirement goals

See Our Social Security Analyzer in Action

Here's what you'll see when you use Praxion's Social Security analyzer. Our tool provides clear visualizations and actionable insights for every claiming decision. Below are three key features that demonstrate the power of comprehensive Social Security analysis.

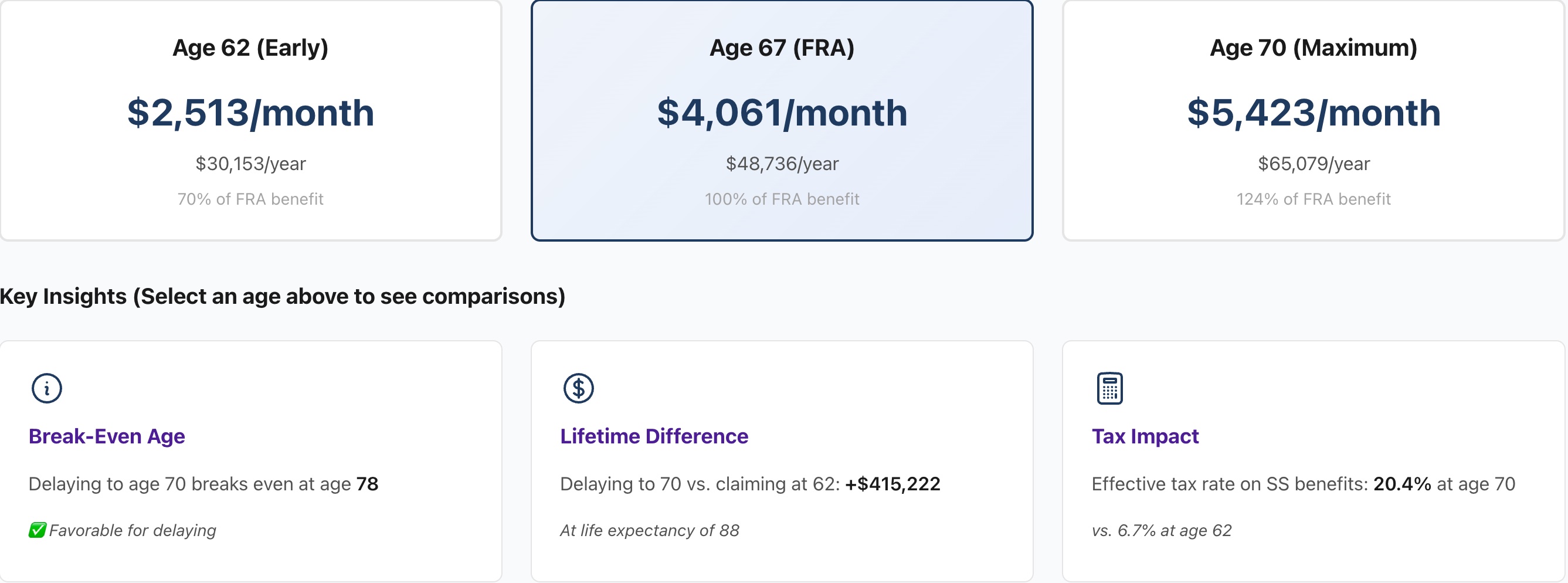

1. Side-by-Side Benefit Comparison

Interactive benefit cards showing monthly and annual Social Security benefits at different claiming ages, plus key insights on break-even age, lifetime difference, and tax impact

What you see: Interactive benefit cards displaying monthly and annual benefits for each claiming age. In this example, the FRA card (Age 67) is selected, showing:

- Age 62 (Early): $2,513/month ($30,153/year) - 70% of FRA benefit

- Age 67 (FRA): $4,061/month ($48,736/year) - 100% of FRA benefit

- Age 70 (Maximum): $5,423/month ($65,079/year) - 124% of FRA benefit

Key Insights displayed: Break-even age (78), lifetime difference (+$415,222 by delaying to 70), and tax impact (20.4% effective rate at age 70 vs. 6.7% at age 62).

2. Break-Even Analysis Chart

Break-even analysis showing when delayed claiming catches up to early claiming, with lifetime benefit differences for each comparison

What you see: Area chart showing cumulative lifetime benefits for each claiming age. The three colored areas represent:

- Age 62 (Red/Pink): Early claiming benefits accumulate quickly but grow slowly

- Age 67/FRA (Blue/Purple): Baseline claiming strategy

- Age 70 (Teal/Green): Delayed claiming starts later but grows faster

Break-Even Points (marked by vertical dashed lines):

- Age 76 (Purple): 62 vs. FRA break-even - FRA catches up to early claiming

- Age 78 (Orange): 62 vs. 70 break-even - Age 70 catches up to age 62

- Age 80 (Cyan): FRA vs. 70 break-even - Age 70 catches up to FRA

Lifetime Differences (at life expectancy of 88):

- 62 vs. 70: +$415,222 by delaying (additional gains after recovery: $435,998)

- 62 vs. FRA: +$263,500 by waiting to FRA (additional gains: $281,355)

- FRA vs. 70: +$151,722 by delaying to 70 (additional gains: $162,687)

✅ With a life expectancy of 88, all comparisons favor delaying—especially waiting until age 70, which provides over $400,000 more in lifetime benefits.

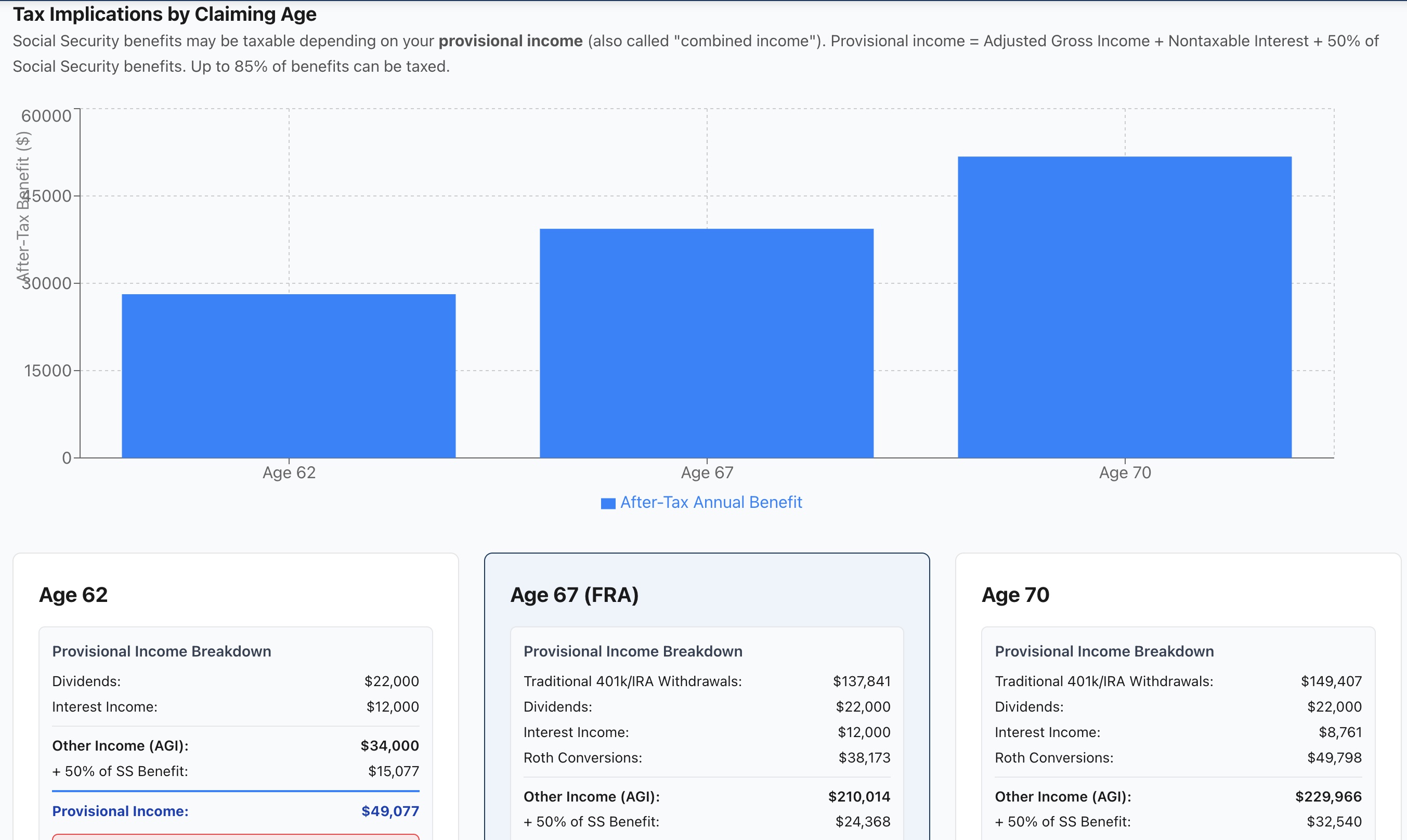

3. Tax Implications Dashboard

Tax implications showing after-tax annual benefits and detailed provisional income calculations for each claiming age

What you see: Comprehensive tax analysis showing how much of your Social Security benefits will be taxable based on your other income sources. The bar chart at top shows after-tax annual benefits:

- Age 62: ~$29,000/year after taxes

- Age 67 (FRA): ~$45,000/year after taxes

- Age 70: ~$56,000/year after taxes

Provisional Income Breakdown (how taxation is calculated):

Each card shows the detailed calculation of provisional income, which determines how much of your Social Security is taxable:

- Dividends + Interest Income

- Traditional 401(k)/IRA Withdrawals (increases at later ages)

- Roth Conversions (if applicable)

- Other AGI (Adjusted Gross Income)

- + 50% of Social Security Benefit

- = Provisional Income

Example from Age 67 (FRA) card:

- Traditional 401k/IRA Withdrawals: $137,841

- Dividends: $22,000

- Interest Income: $12,000

- Roth Conversions: $38,173

- Other Income (AGI): $210,014

- + 50% of SS Benefit: $24,368

- Provisional Income: $234,382

⚠️ Above threshold ($34,000) - 85% of SS taxable

All three ages exceed the threshold, meaning 85% of Social Security benefits are subject to taxation. This is why strategic income planning is critical.

💡 Key Insight: Even though 85% of benefits are taxable at all ages, delaying to 70 still provides significantly higher after-tax income ($56K vs. $29K at age 62)—nearly double the after-tax benefit!

💡 Interactive & Personalized

Unlike static calculators, Praxion's analyzer updates in real-time as you adjust your profile, health factors, or retirement goals. Every number is calculated based on your specific situation—not averages or generic assumptions. The tool also includes opportunity cost analysis and advanced strategies for spousal coordination, tax analysis, and portfolio integration.

Why a Social Security Analyzer is a Game-Changer

Retirement planning isn't one-size-fits-all. Traditional calculators provide generic estimates based on averages, but they don't account for your unique situation. Praxion Finance's Social Security analyzer:

- ✓ Models lifetime benefits: Not just monthly payments

- ✓ Accounts for taxes: Shows after-tax income, not just gross benefits

- ✓ Integrates with investments: Coordinates with your portfolio and withdrawal strategies

- ✓ Models opportunity cost: Shows trade-offs transparently

- ✓ Provides actionable insights: Clear analysis, not just data dumps

- ✓ Considers spousal strategies: Evaluates file-and-suspend, survivor benefits, and coordination

Whether you're considering early retirement, planning around your spouse's benefits, or evaluating investment strategies alongside Social Security, our tool provides the clarity you need to make confident decisions.

Frequently Asked Questions

What is a Social Security analyzer?

A Social Security analyzer is a tool that helps you determine the optimal age to claim Social Security benefits, factoring in life expectancy, taxes, and retirement income goals. It provides personalized analysis based on your unique financial situation.

When should I claim Social Security benefits?

The best age depends on your personal situation. Claiming early at 62 gives immediate income but reduces monthly benefits by up to 30%. Waiting until Full Retirement Age (typically 67) gives 100% of benefits. Delaying until 70 increases benefits by 8% per year. Taxes, investments, health, and life expectancy all influence the optimal timing.

How are Social Security benefits taxed?

Up to 85% of Social Security benefits may be taxable depending on your provisional income (AGI + nontaxable interest + 50% of SS benefits). For single filers: 0% taxable if income < $25,000, 50% if $25,000-$34,000, 85% if > $34,000. For married filing jointly: 0% if < $32,000, 50% if $32,000-$44,000, 85% if > $44,000.

How can I maximize my Social Security benefits?

Use a Social Security analyzer like Praxion Finance's tool to evaluate claiming strategies, consider taxes, understand opportunity costs, and align benefits with your total retirement portfolio. Delaying benefits, managing taxable income, and coordinating with spouse benefits can all increase lifetime value.

Can I combine Social Security with my retirement investments?

Yes! Advanced scenario planning in Praxion Finance allows you to model Social Security alongside investments to model total retirement income. This includes evaluating the opportunity cost of delaying benefits while drawing down investments, and coordinating claiming timing with Roth conversions and other tax strategies.

Is there a free tool to analyze my Social Security options?

Praxion Finance offers a Social Security analyzer that provides personalized, tax-adjusted analysis to help you plan smarter. The tool shows break-even analysis, opportunity costs, and compares claiming at different ages with your complete retirement picture.

Start Maximizing Your Benefits Today

Stop guessing and start planning with confidence. Use Praxion Finance's Social Security analyzer to discover:

- Your optimal claiming age based on life expectancy and goals

- Potential lifetime benefit differences between claiming strategies

- How taxes and opportunity costs affect your retirement income

- Coordination with your investment portfolio and withdrawal strategy

- Break-even analysis and scenario comparisons

Make informed decisions today to secure a financially confident tomorrow.

Try Our Social Security Analyzer Now

See your personalized claiming strategy with tax-adjusted benefits, break-even analysis, and opportunity cost modeling—all integrated with your complete retirement plan.

No credit card required • Full retirement planning included

Note: This article was drafted with AI assistance and reviewed by Praxion Finance experts. Educational purposes only.