Below are the most common reasons projections look unrealistic, and how to create a more grounded plan for your financial future. Understanding these pitfalls can help you identify when a calculator is giving you misleading results and find tools that provide truly realistic projections.

1. Overly Optimistic Investment Returns

Many tools assume a constant 7–10% return every year. That's not how markets work.

In Reality:

- Actual long-term returns after inflation, taxes, and fees are often closer to 2.5–4.5%

- Markets fluctuate — poor early-retirement returns can reduce outcomes dramatically

- Sequence of returns risk: Bad years early in retirement can devastate your portfolio, even if average returns are good

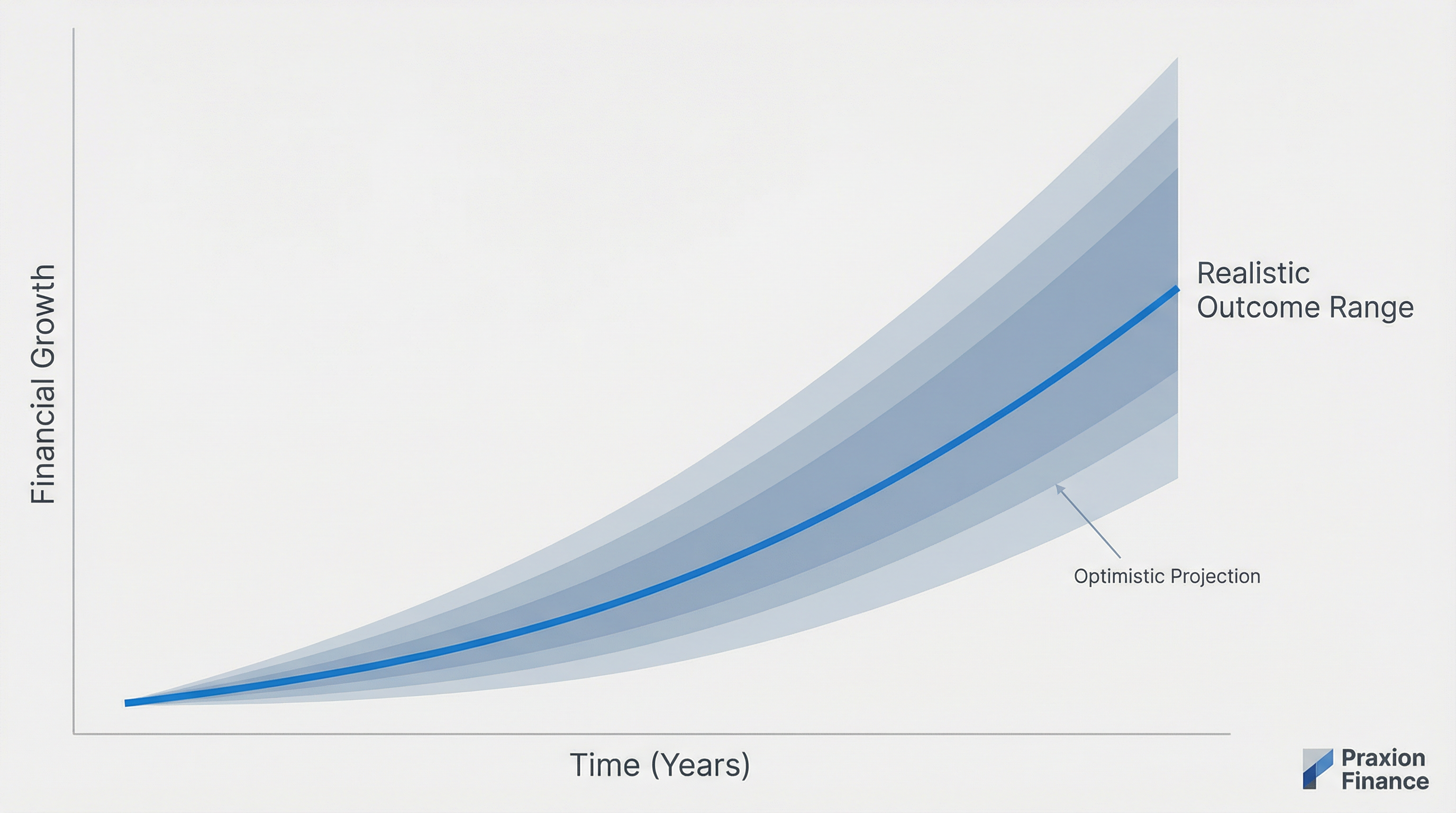

Tip: Ask for projections based on best case, expected case, and downside case scenarios. A realistic tool should show you probability of success, not just one optimistic number.

2. Ignoring Inflation (Or Using the Wrong Rates)

If your income grows 3% but your lifestyle grows 5%, your ability to save shrinks over time. A million dollars today won't have the same purchasing power in 30 years.

Different Expenses Inflate at Different Rates:

- Everyday inflation: ~3%

- Healthcare inflation: 5–6% (significantly higher)

- College costs: 6–7%

- Housing costs: Varies by location

Tip: Ensure inflation is applied to expenses, not just income. Better yet, use different inflation rates for different expense categories.

3. Taxes Are Often Missed or Oversimplified

Before-tax numbers are misleading. Your $500,000 in a traditional 401(k) isn't really $500,000—you still owe taxes on it. Different accounts have different tax treatments that affect your true wealth.

You Must Consider:

- Federal, state, and local taxes

- Payroll taxes (FICA)

- Taxes on investment gains (capital gains, dividends)

- Different taxation for Roth vs Traditional accounts

- Required Minimum Distributions (RMDs) in retirement

Tip: Use after-tax income and after-tax investment returns for planning. A good tool should model your actual tax situation, not just assume a flat rate.

4. Unrealistic Saving Habits

Most tools assume your savings rate stays high for 30+ years. Real life includes major changes that affect your ability to save.

Real Life Includes:

- Starting a family (reduced savings, increased expenses)

- Buying a home (down payment, mortgage, maintenance)

- Career changes (promotions, job loss, career breaks)

- Lifestyle upgrades (as income grows, spending often grows too)

- Supporting aging parents

- Unexpected expenses

Tip: Plan for variable savings rates over time, not one fixed number. Your financial plan should allow you to model different life stages with different savings patterns.

5. Underestimating Healthcare Costs

Healthcare is one of the most significant expenses in retirement, yet many calculators underestimate or ignore it entirely.

The Reality:

- A 65-year-old couple can expect to spend $300,000+ on healthcare in retirement

- Healthcare costs typically inflate at 5–6% annually, much higher than general inflation

- Medicare doesn't cover everything — you'll need supplemental insurance and out-of-pocket costs

- Long-term care costs can add hundreds of thousands more

Tip: Look for tools that model healthcare costs separately with higher inflation rates. Don't rely on calculators that ignore this major expense category.

6. No Risk or Downside Considered

If your calculator gives you one number, it's not realistic. Real planning needs ranges, stress tests, and probability of success.

What's Missing:

- Market volatility — Some years you lose money

- Sequence of returns risk — Bad timing can devastate retirement (poor returns early in retirement deplete principal faster)

- Probability of success — What % of scenarios work out?

- Stress testing — What if you retire during a market crash?

Tip: Look for tools that show you best case, expected case, and worst case scenarios, plus probability of success (e.g., "85% of scenarios show you'll have enough"). Monte Carlo simulations test thousands of possible futures.

7. Social Security Overestimation

People often assume the maximum benefit, even without the earnings history to qualify for it.

Common Mistakes:

- Assuming full benefits without 35 years of work history

- Not accounting for early retirement penalties

- Overestimating spouse benefits

- Ignoring potential future benefit cuts

Tip: Use estimates based on your actual income trajectory. The Social Security Administration provides detailed estimates based on your earnings record.

8. Double-Counting Income Sources

Some calculators count dividends and interest as separate income that reduces what you need to save. But those dividends come FROM your savings!

The Circular Logic Problem:

- "You need $200K because dividends will cover expenses"

- But dividends come from having savings

- So you need more than $200K to generate those dividends

Tip: A good calculator should only count guaranteed income (Social Security, pension, rental income) that's separate from your retirement savings. Asset growth should be handled via discounting, not double-counting.

9. Ignoring Asset Growth During Retirement

Many calculators assume you simply withdraw money and it disappears. In reality, your assets continue to grow during retirement.

The Problem:

- Simple calculators: "You need $4M because expenses × years = $4M"

- Reality: If you have $3M growing at 6%, you need less upfront because growth covers future expenses

Tip: Look for tools that use present value discounting, which accounts for asset growth during retirement. This gives you a more accurate "retirement number."

Bottom Line: What Makes a Realistic Projection

If every person earning $100K ends up a multi-millionaire in your plan, the plan is too optimistic. A realistic projection includes:

- ✅ Taxes — Federal, state, payroll, investment gains

- ✅ Inflation — Different rates for different expense categories

- ✅ Life events — Kids, home purchases, job changes, medical issues

- ✅ Changing savings patterns — Not one fixed savings rate for 30 years

- ✅ Market volatility — Best case, expected case, worst case scenarios

- ✅ Asset growth during retirement — Present value discounting, not simple multiplication

- ✅ Proper income modeling — Only guaranteed income, not double-counting asset returns

A good financial plan is not about predicting the future — it's about preparing for it.

Better Approaches to Retirement Planning

Monte Carlo Simulation

Instead of assuming constant returns, Monte Carlo simulation runs thousands of scenarios with varying market conditions. This gives you a probability of success rather than a single (likely wrong) number.

Year-by-Year Projections

Detailed annual projections show how your income, expenses, and wealth interact over time, accounting for changing tax brackets, Social Security timing, and RMDs.

Historical Stress Testing

See how your plan would have performed during actual historical events like the 2008 financial crisis or the dot-com bust. This shows real-world resilience.

What Praxion Finance Does Differently

Praxion Finance uses sophisticated modeling techniques to address all these common pitfalls:

Federal, state, and local taxes across different account types (Traditional, Roth, Brokerage)

Separate inflation rates for healthcare (5-6%), everyday expenses (3%), and other categories

Model major expenses, career breaks, income changes, and unexpected events

Different savings patterns for different life stages, not one fixed rate

Accounts for asset growth during retirement with proper discounting

Best case, expected case, worst case projections with probability of success

The result is a more realistic picture of your retirement readiness—one that acknowledges uncertainty while helping you plan for it.