1. Introduction

Planned correctly, Roth conversions can supercharge your retirement tax strategy — especially for early retirees. But there's a hidden trade-off that many planners overlook: the intersection of tax brackets, early retirement cash flow needs, and IRA withdrawal restrictions creates narrow windows where conversions are beneficial — and outside those windows they can be costly.

This article dives deep into that trade-off and gives you actionable analysis, visual tools, and technical frameworks to apply to your own retirement plan.

Tax Paid on Roth Conversions by Bracket

See how your tax bracket affects conversion costs

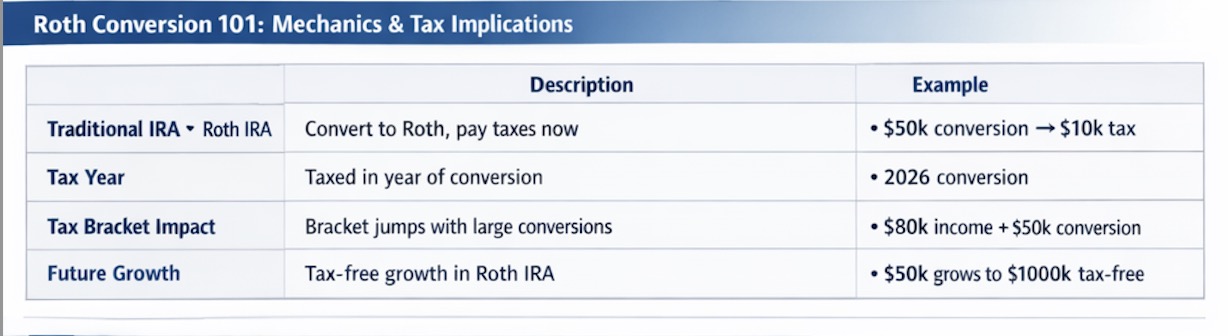

2. Roth Conversion 101: Mechanics & Tax Implications

In simple terms: A Roth conversion window is a period in which converting retirement assets (like a Traditional IRA) to a Roth IRA results in lower lifetime tax costs and improved long-term tax diversification.

✅ A Conversion Window Exists When:

- Your current tax rate is relatively low

- You have cash available to pay the conversion taxes

- You anticipate higher tax rates in the future

⚠️ Warning

Conversions outside these windows can push you into higher tax brackets and reduce net retirement wealth.

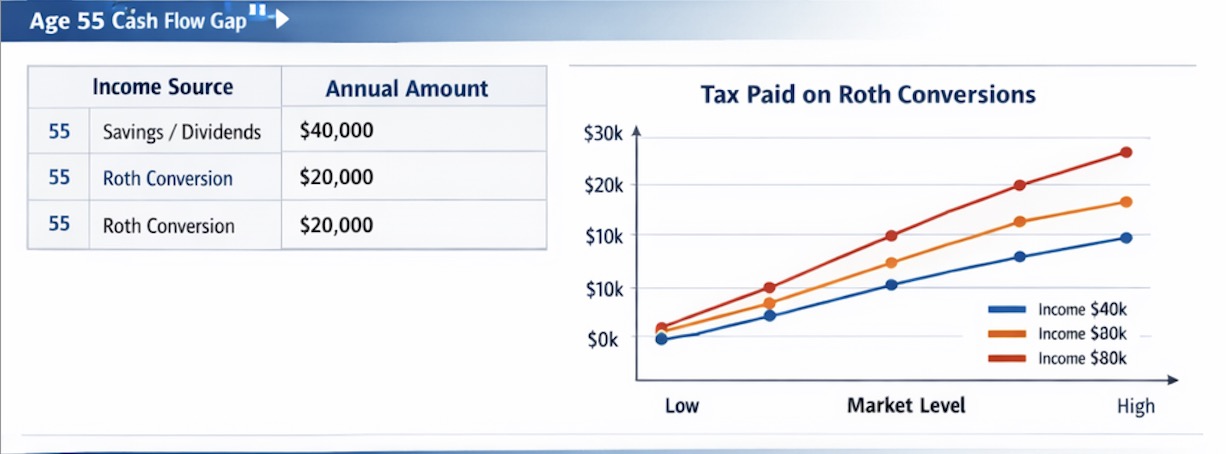

3. Early Retirement Challenges

Unlike conventional retirement at 65+, early retirees (typically ages 50–59½) face unique constraints:

Before age 59½, withdrawals from IRAs/401(k)s incur a 10% penalty. If you have a large taxable (brokerage) account, use that for living expenses first and reserve 401(k)/IRA for Roth conversions—pay conversion taxes from brokerage. Only touch 401(k) for expenses before 59½ if necessary, e.g. via Rule 72(t) (SEPP) to avoid the penalty.

Higher uncertainty in income streams before Social Security or pensions begin

No Medicare until 65, requiring expensive private insurance or ACA subsidies

Modeled withdrawal hierarchy (early retiree with taxable savings)

- Brokerage / cash first — Use for lifestyle and to pay taxes on Roth conversions. Avoids the 10% penalty on 401(k)/IRA.

- Roth conversions every year — Roll 401(k) to Traditional IRA, then convert a chosen amount (e.g. fill 24% or 32% bracket) to Roth; pay the tax from brokerage. Shrinks future RMDs and grows tax-free Roth.

- Traditional 401(k)/IRA last — Only tap for living expenses if brokerage is depleted, or use Rule 72(t) (SEPP) if you must access 401(k) before 59½ without penalty.

All of these factors affect how and when you should harvest tax brackets for conversion.

4. The Tax Mechanics Behind Roth Conversions

When you convert from a Traditional IRA to a Roth IRA, you pay income tax on the converted amount in the year of conversion. The goal is to pay tax now with the expectation that future tax costs will be higher.

Key Factors to Consider:

| Factor | Impact on Conversion Decision |

|---|---|

| Federal Tax Brackets | Convert to fill lower brackets without jumping |

| State Income Tax | Some states have 0% tax on retirement income |

| Medicare IRMAA | High conversion income can trigger premium surcharges |

| AMT Considerations | Large conversions may trigger Alternative Minimum Tax |

| Capital Gains Interaction | Conversion income stacks with other income for cap gains rates |

The Single Filer Penalty

If you file as single (or head of household with similar bracket widths), federal tax brackets are half as wide as for married couples filing jointly — not merely “half the income.” The 24% bracket, in particular, spans a much narrower band of taxable income for singles than for couples. That means “bracket-topping” conversions — filling the space to the top of a target bracket without spilling into the next — require more precision for single filers: a modest overshoot can push a large slice of your conversion into the 32% bracket (and higher), eroding the benefit you were trying to capture.

For couples, the same dollar conversion often sits comfortably in the 24% zone; for a single filer with similar lifestyle costs, the same strategy can behave like a tightrope. Use multi-year projections and slice conversions into smaller annual amounts rather than assuming one-size-fits-all “fill the 24% bracket” rules from joint-filer examples.

Takeaway: Single filers should treat bracket-topping as a precision exercise. When in doubt, convert less per year and extend the Roth conversion window — especially if you are also navigating IRMAA, capital gains, or state tax cliffs.

6. Key Conversion Strategies Before Age 59½

Technical planners often suggest these strategies:

A. Bucket Conversions

Break annual conversions into slices to manage bracket creep. Convert just enough to fill your current tax bracket without jumping to the next one.

B. Income Smoothing

Use taxable accounts to fill income up to the top of a tax bracket before converting.

C. Sequence Retirement Withdrawals

Leverage the optimal order: Taxable portfolio first → Then Roth conversions to fill lower brackets → Then tax-deferred accounts.

D. Use Monte Carlo + Tax Simulations

Combining dynamic modeling yields better timing decisions. Test your conversion strategy under thousands of market scenarios.

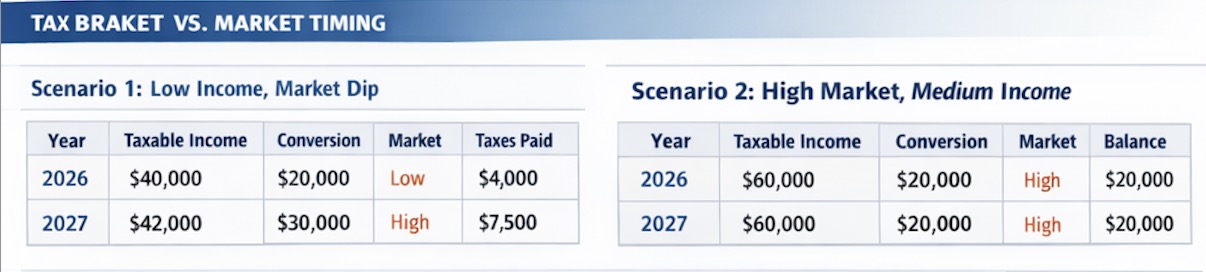

7. Data-Driven Roth Conversion Scenarios

Scenario 1: Low Income, Market Dip

| Year | Taxable Income | Conversion | Market | Taxes Paid | Roth Balance EOY |

|---|---|---|---|---|---|

| 2026 | $40,000 | $20,000 | Low | $4,000 | $20,000 |

| 2027 | $42,000 | $30,000 | Medium | $6,600 | $52,000 |

| 2028 | $45,000 | $25,000 | Low | $5,000 | $82,000 |

✅ Outcome: Waiting for market dips and managing bracket fills improved after-tax outcome by converting more shares at lower prices.

Scenario 2: High Market, Medium Income

| Year | Taxable Income | Conversion | Market | Taxes Paid |

|---|---|---|---|---|

| 2026 | $60,000 | $20,000 | High | $5,000 |

| 2027 | $65,000 | $30,000 | High | $8,000 |

⚠️ Outcome: Higher income + high market valuations = paying more tax for fewer converted shares. Consider waiting for better conditions or reducing conversion amounts.

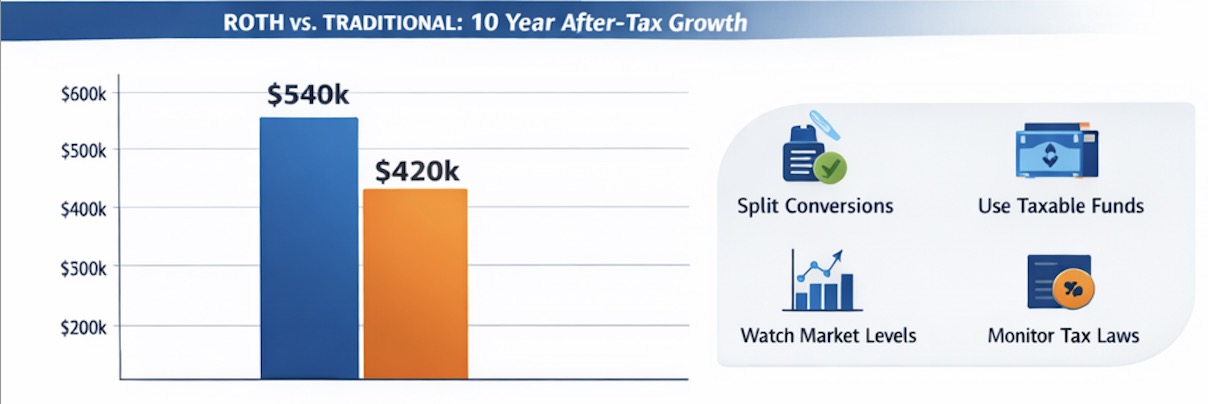

Roth vs Traditional IRA: 10-Year After-Tax Growth

$100k starting balance, 7% annual return, 22% tax on Traditional withdrawals

8. Visual Analysis: Conversion Windows & Market Timing

Roth Conversion "Sweet Spot" Finder

Conversion opportunity score by income level and market conditions

The Sweet Spot: Low Income + Low Market

Converting when both taxable income AND market valuations are low maximizes your after-tax wealth. Early retirement years (ages 55-59) often create this ideal window.

Roth vs Traditional: 10-Year After-Tax Growth

Early strategic conversions outperform late lump conversions, even if total contribution is the same. The key is maximizing tax-free growth years in the Roth account.

9. Pitfalls and Risks

🚨 Common Missteps

| Risk | Description | Mitigation |

|---|---|---|

| Bracket Creep | Converting too much in one year | Slice conversions over multiple years |

| Market Timing | Converting at peak valuations | Monitor indices, use partial conversions |

| Early Withdrawal Penalty | Using IRA funds to pay conversion tax | Fund conversion taxes with cash |

| Medicare IRMAA | High conversion income increases premiums | Smooth conversions to avoid thresholds |

⚠️ Unexpected Risks

- Market volatility — valuations can swing dramatically year to year

- Policy changes — potential changes to retirement tax laws

- Alternative Minimum Tax (AMT) — large conversions may trigger AMT

- State tax changes — moving states can affect optimal strategy

10. Actionable Steps for Early Retirees

- Simulate forward — project income, Roth conversions, and tax brackets using Monte Carlo simulations

- Identify windows — find years where taxable income is low and expected future rates are higher

- Use taxable reserves — pay conversion tax with cash rather than IRA funds

- Watch for market dips — convert when valuations are low

- Avoid Medicare premium spikes — smooth conversions to stay below IRMAA thresholds

- Analyze with our tools — use the Roth Conversion Analyzer and Tax Optimizer

Ready to Find Your Optimal Conversion Window?

Use Praxion Finance to simulate Roth conversion strategies, including market impact and bracket creep analysis.

Conclusion

The interplay between early retirement cash flow needs, market timing, and tax bracket navigation creates a nuanced trade-off when planning Roth conversions. Properly identifying conversion windows maximizes after-tax wealth and accelerates tax-free growth.

With thoughtful modeling, early retirees can unlock hidden value in these windows and avoid costly mistakes. The key is combining income analysis, market awareness, and multi-year tax planning into a cohesive strategy.

Frequently Asked Questions

Q: What is the best age to do Roth conversions?

Typically before age 59½ during low-income years. Early retirement creates an ideal window because income is often lower before Social Security and RMDs begin.

Q: Do Roth conversions affect Social Security taxes?

Yes — conversions count as taxable income, impacting provisional income which determines how much of your Social Security benefits are taxable.

Q: Should I convert all at once?

No — spreading conversions over multiple years usually improves tax efficiency by avoiding bracket creep.

Q: Can I do Roth conversions before age 59½?

Yes, you can convert at any age. However, the funds used to pay conversion taxes should come from outside the IRA to avoid early withdrawal penalties.

Q: How does market timing affect Roth conversions?

Converting when market valuations are low means you pay tax on a smaller balance, effectively converting more shares for less tax. This creates a trade-off with income timing.

Q: Why is Roth conversion harder for single filers?

Federal brackets for single filers are much narrower than for married couples filing jointly. The 24% bracket spans a smaller band of taxable income, so bracket-topping conversions require more precision—overshooting can push a large part of the conversion into the 32% bracket or higher.

Q: Should I keep extra cash in brokerage when doing Roth conversions?

Yes. Maintain a volatility buffer—cash or stable holdings—to pay conversion taxes and spending without selling long-term investments during a downturn. Otherwise sequence-of-returns risk can force sales at bad prices and undermine careful tax planning.