1. Why War Is a Retirement Risk

Retirement planning models inflation, longevity, taxes, and market volatility. Very few plans explicitly account for war. Yet history shows that geopolitical conflict — even when fought far from U.S. soil — can alter market returns, inflation regimes, tax policy, interest rates, and the timing of retirement in ways that materially change lifetime financial outcomes.

The impact is rarely about permanent market collapse. Diversified portfolios have survived every major conflict of the past century. The real risks are more subtle: sequence of returns, inflation shocks, tax policy shifts, and the behavioral mistakes made under fear.

This article examines four historical conflicts with real market data, shows how retirement timing relative to each conflict shaped lifetime outcomes, and provides a structural framework to build a plan resilient to geopolitical uncertainty.

Key insight: War does not automatically destroy retirement plans. But it amplifies weaknesses already present in them. If your plan only works in calm markets, low inflation, and stable tax regimes — it is not resilient.

2. Case Study: World War II (1939–1945)

World War II remains the most studied geopolitical shock in market history — and the results are more nuanced than most investors expect.

Market Behavior

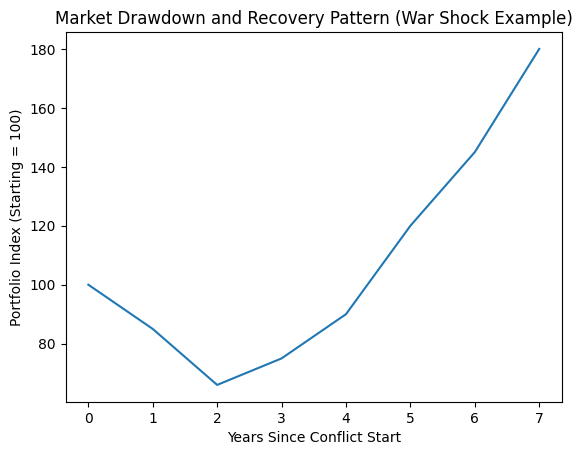

From their pre-war highs, U.S. equities fell approximately 34% peak to trough by April 1942. The bottom came not at war's end, but while the conflict was still intensifying. From that April 1942 low, the market recovered approximately 67% through the end of the war in August 1945 — a powerful rally that rewarded investors who stayed the course.

The S&P 500 in its modern form did not exist until 1957, but U.S. equity market indices of the era show the full-period gain from September 1939 to August 1945 was approximately +38% — a positive return across the entire war.

The Real Damage: Post-War Inflation

The war itself was survivable. What followed was more damaging for retirees. As wartime price controls were removed, inflation surged sharply:

- 1946: 8.3% inflation

- 1947: 14.4% inflation — the most damaging year

- 1948: 3.0% (deceleration)

- Cumulative 1946–1947: approximately 27% purchasing power erosion

Three Retirement Cohorts

Suffered early drawdown, but benefited from the 1942–1945 market rally. Post-war inflation eroded purchasing power. Manageable if withdrawals were flexible.

One of the best retirement cohorts in history. Entered at market lows and captured the full 67% recovery through 1945 and beyond.

Faced the worst outcome. 14.4% inflation in 1947 immediately eroded purchasing power. Required rising withdrawals from day one with no buffer rally ahead.

See how sequence risk affects your specific plan

Run a personalized stress test to see how a WWII-style early drawdown would impact your projected retirement.

3. Case Study: Vietnam War Era & Yom Kippur Shock (1973–1974)

This period produced the most damaging retirement environment of the modern era. But the causation matters: the Vietnam War itself did not directly crash markets. Its multi-year financing through deficit spending and monetary expansion built a foundation of inflationary pressure. The direct crash trigger came from a separate conflict.

In October 1973, Arab petroleum exporters imposed an oil embargo on the United States following Nixon's request for emergency aid to Israel during the Yom Kippur War. Oil prices nearly quadrupled — from $2.90 to $11.65 per barrel — within months.

Market & Inflation Impact

- S&P 500 fell approximately 45% from January 1973 to December 1974

- The DJIA lost more than 45% over the same period

- Inflation in 1974: 12.3%

- The "Great Inflation" era (1965–1982) peaked at approximately 14–15% in March 1980

- Bonds also declined as interest rates rose sharply — there was no traditional safe haven

Stagflation: The Worst Combination

Stagflation — falling stocks, falling bonds, and rising inflation simultaneously — is the most destructive environment for a retirement portfolio. Every asset class fails at once while withdrawal needs rise. The 1973 retiree faced all three simultaneously.

Retirees who began withdrawals in 1973 faced decades of recovery. Many had to reduce spending significantly, re-enter the workforce, or delay planned retirement. Historical analysis shows the U.S. equity market did not return to pre-crash real (inflation-adjusted) levels until the early 1990s — a nearly 20-year period of impairment for those who retired at the worst time.

4. Case Studies: Gulf War (1990) & Russia-Ukraine (2022)

Gulf War (1990–1991): Short Conflict, Limited Structural Damage

Following Iraq's invasion of Kuwait on August 2, 1990, the S&P 500 declined approximately 19% from its July 1990 peak to its October 1990 trough — a sharp but contained drop. The market recovered quickly, and 1991 ended as a strongly positive year for equities.

The Gulf War illustrates an important historical pattern: short, geographically contained conflicts with limited inflation spillover typically produce temporary market volatility, not structural retirement damage. A retiree who held their allocation through 1990–1991 experienced discomfort, not portfolio ruin.

Russia-Ukraine War (2022): 1970s Dynamics, Modern Portfolios

While Russia's invasion of Ukraine in February 2022 was not a global war, its economic effects were significant and structurally resembled the 1970s more than the Gulf War:

- S&P 500: –18.1% for calendar year 2022

- Bloomberg U.S. Aggregate Bond Index: –13% — the worst year for bonds since the index's inception in 1976

- U.S. inflation: peaked at 9.1% in June 2022, the highest reading since November 1981

- A traditional 60/40 portfolio lost approximately 16% — the third worst year ever for diversified investors, and the first time ever both stocks and bonds simultaneously fell more than 10%

Key lesson from 2022: The traditional assumption that bonds offset equity losses breaks down when war drives inflation. In 2022, holding more bonds made the problem worse, not better. Retirees who began withdrawals in January 2022 experienced immediate sequence-of-returns stress.

Chart: Markets often bottom before wars end. The danger for retirees is not the war itself — it is withdrawing from a declining portfolio before the recovery arrives.

5. Sequence Risk: Timing Is Everything

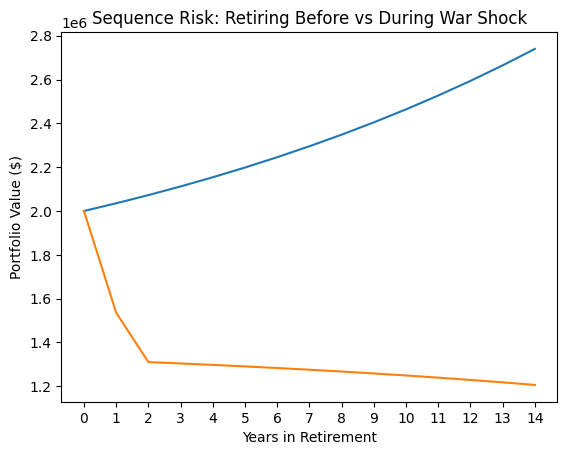

The same war. The same market decline. The same eventual recovery. Completely different retirement outcomes — depending entirely on when you retired relative to the shock. This is sequence-of-returns risk, and it is the most underappreciated retirement danger in geopolitical scenarios.

Consider three retirees with identical portfolios: $2,000,000 in a 60/40 allocation, withdrawing 4% annually ($80,000).

Portfolio built a buffer during the pre-conflict growth period. Has embedded gains that absorb the initial drawdown. Withdrawal amounts remain manageable relative to portfolio size. High long-term survival probability.

Faces an immediate 15–30% portfolio decline in the first year of withdrawals. Must sell more shares at depressed prices to fund the same $80,000 withdrawal. Inflation simultaneously increases the real cost of living. Portfolio longevity is meaningfully reduced — even if long-term average returns are identical to Retiree A.

Outcome depends heavily on whether the inflation episode has resolved. If markets have recovered and inflation has cooled (e.g., Gulf War pattern), outcome is favorable. If inflation persists for years (e.g., 1970s pattern), continued stress on withdrawals.

Chart: Same long-term average return. Same withdrawal amount. The sequence of early returns determines whether the portfolio lasts a lifetime — or doesn't.

Concerned about sequence risk in your plan?

View your year-by-year projections to see exactly how early market shocks affect your long-term balance.

6. Inflation: The Hidden Threat

Across every major conflict examined, inflation — not the initial market drop — has caused the most lasting retirement damage. War disrupts the supply chains that underpin price stability: energy production, food distribution, shipping routes, and manufacturing inputs.

Retirees are uniquely vulnerable because they have no wage growth to offset rising prices. A worker who earns $120,000 may receive a 5% raise when inflation runs at 6%. A retiree drawing $80,000 annually must either withdraw more from a declining portfolio or accept a lower standard of living.

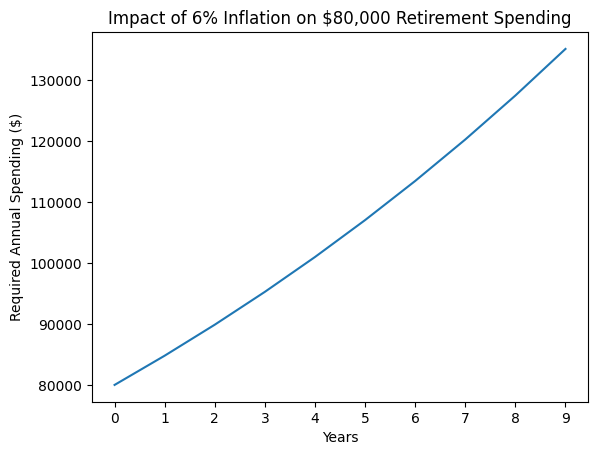

The Compounding Cost of 6% Inflation on an $80,000 Lifestyle

At 6% annual inflation, what cost $80,000 in Year 1 costs over $143,000 by Year 10 — requiring a 79% increase in annual withdrawals over a decade.

Historical war-period inflation has ranged from 5% to 15% — dramatically above the 2–3% most retirement plans assume. Even a sustained 5% inflation for five years produces compounding withdrawal pressure that many fixed-rate plans cannot absorb.

Chart: At 6% inflation, an $80,000 retirement lifestyle requires over $191,000 annually within 15 years — nearly 2.4x the original withdrawal amount.

7. Long-Term Structural Effects of War

1. Higher Government Debt → Future Tax Pressure

Wars are expensive and are historically financed through a combination of debt issuance, monetary expansion, and tax increases. During World War II, the top marginal federal income tax rate reached 94% in 1944–1945 on income above $200,000 (equivalent to approximately $3.6 million today). Today, with federal debt already at historically elevated levels, a prolonged conflict increases the probability of:

- Higher future marginal income tax rates

- Changes to capital gains treatment

- Modifications to retirement account rules or benefit calculations

- Means-testing of Social Security and Medicare benefits

For individuals holding large Traditional 401(k) or IRA balances — where every dollar of future withdrawal is taxed as ordinary income — war meaningfully increases tax risk. This strengthens the case for proactive Roth conversion strategies before geopolitical shocks materialize.

War increases the probability of future tax rate increases

Roth diversification now creates flexibility regardless of what tax policy looks like in 20 years.

2. Bond Market Correlation Shift

The traditional 60/40 portfolio relies on a fundamental assumption: when stocks fall, bonds rise and offset losses. This held true through most recessions of the past 40 years. War-driven inflation breaks this relationship.

In 2022, both the S&P 500 (–18.1%) and Bloomberg Aggregate bonds (–13%) fell simultaneously — the first time in history that both fell more than 10% in the same calendar year. A traditional 60/40 portfolio lost approximately 16%, the third worst year ever for diversified portfolios. Retirees who held more bonds in 2022 were not safer — they were more exposed.

3. Sector & Geographic Reallocation

Wars redirect capital. Sectors that historically benefit during conflict include defense contractors, domestic energy producers, commodity exporters, and cybersecurity firms. Sectors under pressure typically include airlines and travel, global trade-dependent companies, and emerging market equities.

For retirees with concentrated positions in global growth equities — a common outcome for technology professionals with large RSU or ESPP accumulations — geopolitical realignment can produce valuation compression that outlasts the conflict itself.

8. Who Is Most Exposed?

Not all retirees face equal geopolitical risk. The structural characteristics of a retirement plan determine how much damage a war-driven shock can do.

Higher Vulnerability

- Retiring within 5 years

- Fixed 4% withdrawal with no flexibility

- No cash reserve or liquidity buffer

- Large Traditional IRA/401(k) with no Roth diversification

- Heavy bond allocation during rising-rate environment

- Over-concentrated in global growth equities

More Resilient

- Flexible withdrawal strategy tied to performance

- 2–3 year expenses in cash or short-term instruments

- Tax-diversified accounts (Traditional + Roth + Brokerage)

- Inflation-aware asset allocation

- Optional flexibility in retirement timing

- Multiple income sources (Social Security, pension, part-time)

9. Mitigation Strategies

You cannot predict war. You can build structural resilience so that your retirement plan does not depend on peace.

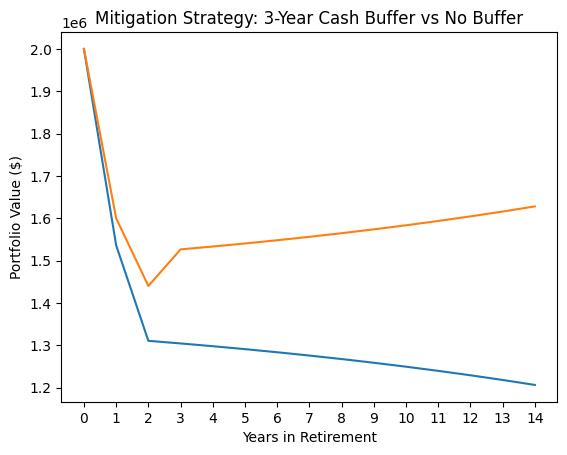

1. 2–3 Year Cash Buffer

Hold 2–3 years of living expenses in cash or short-term Treasury instruments. This prevents forced equity sales during drawdowns, which is the primary mechanism through which sequence risk permanently damages portfolios. A cash buffer allows equities to recover before withdrawals resume. Research consistently identifies this as one of the highest-impact single actions a retiree can take.

2. Dynamic Withdrawal Guardrails

Replace a fixed annual withdrawal rate with guardrail-based flexibility. When the portfolio declines beyond a threshold (typically 15–20%), reduce withdrawals by 10–15%. When the portfolio recovers above a ceiling, allow increases. This simple adjustment meaningfully improves portfolio longevity across war, recession, and stagflation scenarios.

3. Tax Diversification

Blend Traditional (pre-tax), Roth (tax-free), and taxable brokerage accounts. War increases the probability of future tax reform. A portfolio with all assets in tax-deferred accounts has no flexibility if tax rates rise. Roth accounts provide tax-free withdrawals regardless of future policy — and Roth conversions are most efficient during lower-income years before retirement.

4. Inflation-Aware Asset Allocation

Consider structural exposure to assets with pricing power: domestic energy, real assets, commodities, TIPS (Treasury Inflation-Protected Securities), and dividend-growing equities in inflation-resilient sectors. This is not speculation — it is diversification against the specific risk that war most reliably produces. A small allocation (10–15%) to inflation-sensitive assets can meaningfully buffer war-driven inflation episodes.

5. Retirement Timing Flexibility

Delaying retirement by even 12–24 months during an active conflict or severe market downturn can substantially change lifetime outcomes. Working longer allows market recovery before withdrawals begin, increases Social Security benefits (approximately 8% per year of delay from 62 to 70), and reduces the total years the portfolio must fund. Across historical conflict periods, timing flexibility has offset most of the damage from early sequence risk.

Chart: A 3-year cash buffer prevents forced portfolio sales during war-driven drawdowns, meaningfully improving long-term portfolio survival without requiring any market-timing decisions.

Praxion Finance

Is your retirement plan resilient to geopolitical shocks?

Run a free, personalized analysis to see how war-driven scenarios — inflation, sequence risk, and tax changes — would impact your specific plan.

Run Your Own War Stress Test

These exact scenarios are already built into Praxion Finance. See how your specific portfolio — your savings, income, and withdrawal plan — would have performed through each one.

- S&P 500: –45%

- Inflation peaked >14%

- Bonds also declined

- Worst modern cohort

- S&P 500: –18.1%

- Bonds: –13%

- CPI peaked 9.1%

- 60/40 lost ~16%

Free to start · No credit card required

Frequently Asked Questions

Does war always cause a stock market crash?

Not always, and not permanently. Markets often fall sharply at the onset of conflict but historically recover — sometimes before the war ends. During WWII, the U.S. market bottomed in April 1942 and rallied approximately 67% through war's end. The greater long-term risk for retirees is typically inflation and the sequence of returns, not the initial market drop.

What is sequence of returns risk and why does it matter during war?

Sequence of returns risk is the danger that poor market returns early in retirement — while you are making withdrawals — permanently impair your portfolio. War-driven downturns are especially dangerous because they can trigger a 15–30% decline in the first years of retirement, forcing you to sell more shares at lower prices. Even if markets recover, the portfolio never fully catches up.

How does war-driven inflation affect retirees specifically?

Retirees are hit harder than workers because they have no wage growth to offset rising prices. An $80,000 retirement lifestyle under 6% inflation grows to $101,000 in just four years and over $143,000 in ten years. War periods have historically produced inflation ranging from 5% to 15% — well above the 2–3% most retirement plans assume.

What is a guardrail withdrawal strategy?

A guardrail withdrawal strategy replaces a fixed annual withdrawal rate (like the 4% rule) with a flexible approach tied to portfolio performance. When the portfolio declines significantly, withdrawals are reduced by 10–15%. When the portfolio recovers above a certain threshold, withdrawals can increase. This approach meaningfully improves portfolio longevity during volatile markets — including war-driven downturns.

Should I move to cash if a war starts?

Almost certainly not. Moving entirely to cash is one of the most historically damaging decisions a retiree can make. Markets often bottom during — not after — conflicts, and investors who exit miss the recovery. The behavioral impulse to "get safe" during geopolitical crises has done more damage to retirement portfolios than the wars themselves. A better approach is to already hold a 2–3 year cash buffer before any crisis, so you never need to sell equities at the worst time.

What History Actually Shows

Across four major conflicts spanning 85 years, a consistent pattern emerges: markets recover, but inflation and sequence risk determine which retirees survive intact.

| Conflict | Market Impact | Inflation | Worst Cohort | Key Lesson |

|---|---|---|---|---|

| WWII (1939–1945) | –34%, then +67% recovery | 14.4% peak (1947) | 1946 retirees | Post-war inflation > war itself |

| Vietnam / 1970s | –45% (1973–74) | ~14–15% peak (1980) | 1973 retirees | Stagflation is worst case |

| Gulf War (1990) | –19%, quick recovery | Minimal spillover | Limited impact | Short wars = temporary volatility |

| Ukraine / 2022 | –18% stocks, –13% bonds | 9.1% peak (June 2022) | 2022 retirees | 60/40 failed; 1970s dynamics |